Choosing a bank as a startup comes down to a handful of concrete questions: What does the account cost each month? How much of your balance is actually FDIC-insured — and which chartered bank holds the money? What does idle cash earn? Can you deposit cash if your business handles it? And when a six-figure wire goes wrong, does a human pick up the phone?

This guide compares 18 banks and fintech platforms on exactly those numbers — monthly fees, FDIC coverage limits, yield (as-of dated), cash-deposit support, and the bank behind each platform, including its size — with every figure sourced and dated.

On those criteria, Rho is the strongest fit for venture-backed startups in 2026: $0 monthly fees; checking held at Webster Bank, N.A. — an $85.5B-asset national bank (FDIC call report, 3/31/2026), the largest deposit partner bank of any major US business-banking fintech; savings with up to $75M in FDIC insurance through American Deposit Management Co.'s network of 400+ insured institutions; treasury yield of up to 4.55% (as of 08/03/2026) from a $100,000 minimum — less than half Mercury's $250,000; and 24/7 human support by phone or chat on every account.

Most founders don't think much about banking until something breaks. Then they're mid-fundraise, payroll is due, and their banking platform is a ticket queue and a CSV export. The question isn't whether to choose a better platform — it's whether to choose one before you need it or after. Rho is built for founders from day one: open an account in minutes, issue cards, and start earning yield on idle cash before your first wire hits — and the platform you open on day zero is the same one your controller runs at Series B.

For founders already on a basic account and staring at a raise, this is the second-best time to make the switch. Here's how 18 platforms compare on what matters once real money is involved: FDIC coverage, treasury yield, AP automation, and integrations that keep your books clean as you scale.

Key Takeaways:

Best overall for venture-backed startups: Rho — $0 monthly fee; checking at Webster Bank, N.A. ($85.5B in assets, FDIC 3/31/2026); savings with up to $75M FDIC insurance via a 400+ bank sweep network; treasury yield up to 4.55% (as of 08/03/2026) from a $100,000 minimum; 24/7 human phone and chat support on every account.

FDIC coverage is the widest gap in the table: $250K standard at any single bank vs. $3M–$75M on sweep-network products (coverage is per product — e.g., Rho's $75M applies to savings; its checking, like everyone's, is insured to $250K at the bank that holds it). If you're holding more than $250K post-raise, coverage math should shortlist your options before features do.

Ask which bank actually holds your money. A fintech platform is a technology company, not a bank — deposits sit at partner banks that range from $642M to $85.5B in total assets across this list (FDIC call reports, 3/31/2026). The partner bank's identity and size are public facts you can verify, and they belong in the decision.

The monthly fee isn't the total cost: wires ($0–$50 each), same-day ACH ($0 to 1%/txn), per-user software fees ($0–$15/user), and paid feature tiers separate platforms that all advertise “$0 to start.”

Cash businesses need a different shortlist: most startup fintechs (Rho, Mercury, Brex, Ramp) don't accept cash deposits; traditional banks and a few fintechs with retail/ATM networks do.

The best time to open an account is at incorporation — before payroll, vendors, and a finance team make switching painful; the most expensive mistake is choosing a platform that's right for today and wrong for 18 months from now.

While many startups use Rho to manage their business banking, Rho is a fintech company, not a bank. Rho partners with FDIC-insured banks to offer banking products and services. Applying will not impact your personal credit score.

Competitive data verified as of August 2, 2026 (bank total assets from Q1 2026 FDIC call reports; yields as-of dated per cell). Subject to change.

Platform | Monthly fee (base plan) | Yield / APY (as-of) | Max FDIC coverage | Cash deposits | Deposits held at | Bank total assets (as of) | Files your C-corp? |

|---|---|---|---|---|---|---|---|

Rho | $0 — no monthly, per-user, or platform software fees | Treasury up to 4.55% (08/03/2026), $100K minimum — securities, SIPC not FDIC | Savings: up to $75M via ADM’s 400+ bank sweep network. Checking: $250K (Webster) | No | Webster Bank, N.A. (checking/cards); ADM Co. + partner banks (savings) | $85.5B (03/31/2026, FDIC) | Yes — free* |

Mercury | $0 base; from $29.90/mo (Plus) and $299/mo (Pro); annual billing is lower | Checking/savings: none. Mercury Treasury (min $250K): 3.01%–3.81% net by tier (07/27/2026) — securities, SIPC not FDIC | Up to $5M via sweep across up to ~20 program banks (checking/savings) | No | Choice Financial Group + Column, N.A. (own charter conditionally approved by OCC Apr 2026; not yet operating) | Choice $6.13B; Column $1.39B (03/31/2026, FDIC) | No |

Brex | $0 base (Essentials); Premium $12/user/mo | 4.01%–4.36% via money market fund (as displayed 07/31/2026) — securities, SIPC not FDIC | Checking: $250K (Column). Vault: up to $6M via ~24 program banks | No | Column, N.A. (checking); Vault via program banks | $1.39B (03/31/2026, FDIC) | No |

Bluevine | $0 Standard; $30 Plus; $95 Premier | 1.3% Standard (to $250K, activity reqs) / 1.75% Plus / 3.0% Premier (displayed 08/02/2026) | Up to $3M via Coastal + ~17-bank sweep | Yes — Green Dot retail (fee up to $4.95); Allpoint+ ATMs ($1 + 0.5%) | Coastal Community Bank | $5.66B (03/31/2026, FDIC) | No |

Relay | $0 Starter; $30 Grow; $90 Scale | Savings only: 1.11% / 1.75% / 3.00% by plan (as of 05/01/2026) | Up to $3M via Thread Bank insured-cash-sweep | Yes — free at Allpoint+ ATMs ($1,000/txn); Green Dot retail (fee up to $4.95) | Thread Bank | $1.04B (03/31/2026, FDIC) | No |

Ramp | $0 base; Plus $15/user/mo + platform fee (amount not published) | 2% APY on checking; Investment Account up to 4.33% (ramp.com, 08/02/2026) — securities, not FDIC-insured | IntraFi ICS sweep via FIB — “up to the maximum allowed by law”; no headline dollar cap published | No | First Internet Bank of Indiana | $5.68B (03/31/2026, FDIC) | No |

Grasshopper | $0 | 1.00%–1.35% checking APY by balance tier (rates eff. 11/03/2025, fetched 08/02/2026) | $250K standard; up to $125M via ICS sweep | Select MoneyPass ATMs | Grasshopper Bank, N.A. (direct bank) | $1.53B (03/31/2026, FDIC) | No |

Wells Fargo | $15 (Initiate); $15–$75 tiers; waivable | 0% on entry checking (Navigate tier interest-bearing, rate unpublished) | $250K standard | Yes — branches/ATMs; first $5K/period free, then $0.30 per $100 | Wells Fargo Bank, N.A. (direct bank) | $1.85T (03/31/2026, FDIC) | No |

JPMorgan Chase | $15 (Business Complete); $15–$95 tiers; waivable | 0% — business checking does not earn interest (2026 fee schedule) | $250K standard | Yes — ATM unlimited free; $5K/period teller-free, then 0.30% | JPMorgan Chase Bank, N.A. (direct bank) | $4.02T (03/31/2026, FDIC) | No |

Bank of America | $16 (Fundamentals, $0 first 12 mo); $16–$29.95 tiers; waivable | 0% — business checking is non-interest-bearing | $250K standard | Yes — branches/ATMs; first $5K/cycle free, then $0.30 per $100 | Bank of America, N.A. (direct bank) | $2.67T (03/31/2026, FDIC) | No |

Axos | $0 (Basic); $0–$10 tiers | Up to 1.01% APY on interest checking, ≤$50K balances (as of 08/02/2026) | $250K standard; up to $265M via IntraFi ICS (per Axos site 08/02/2026) | ATM cash deposits (MoneyPass/AllPoint) | Axos Bank (direct bank) | $28.2B (03/31/2026, FDIC) | No |

Live Oak Bank | $10 (Essential, waivable); $10–$100 tiers | Business savings 2.85% APY (08/02/2026); checking non-interest | $250K standard; ICS sweep available ($350K min; no dollar cap published) | No — fully digital, cash not accepted | Live Oak Banking Company (direct bank) | $15.2B (03/31/2026, FDIC) | No |

HSBC Innovation Banking | $0 first 24 months (Spark, Series A and earlier); Innovation package waived at $1.8M avg balance | Money market rate not published | $250K standard; expanded via Distributed Deposits network (no dollar figure published) | Not published | HSBC Bank USA, N.A. (direct bank) | $167.7B (03/31/2026, FDIC) | No |

Novo | $0 | None — non-interest checking (08/02/2026) | $250K standard only — no sweep product | No — money-order + mobile check deposit workaround only (third-party-sourced) | Middlesex Federal Savings, F.A. | $642M (03/31/2026, FDIC) | No |

US Bank | $0 (Silver); $0–$30 tiers; waivable | 0% on entry checking | $250K standard | Yes — branches/ATMs; 25 free cash-deposit units/cycle | U.S. Bank, N.A. (direct bank) | $683B (03/31/2026, FDIC) | No |

SVB (division of First Citizens Bank) | $0 first 3 years (Edge), then $50/mo; ScaleUp $50 waivable | Startup Money Market 0.10%–3.30% APY by balance tier (rate sheet dated 12/10/2025) | $250K standard; multi-million via IntraFi ICS (no cap published) | Via First Citizens branches (not published for SVB accounts) | First-Citizens Bank & Trust Company (direct bank) | $235.5B (03/31/2026, FDIC) | No |

Found | $0 base; Plus $35/mo or $315/yr; Pro $80/mo (per third-party reviews, 2026 — found.com blocks automated verification) | Base: none; Plus 1.50% (to $20K); Pro 2.50% (third-party, 2026) | $250K standard | Yes — retail partners via app, $2.00/deposit (third-party, 2026) | Lead Bank (new/current accounts) + Piermont Bank (legacy accounts) | Lead: $2.68B (03/31/2026, FDIC) | No |

Stifel | Not published — contact for pricing | Not published (“high yield” on Stifel Bank deposits) | Up to $225M per insurable capacity via IntraFi ICS (per Stifel site, 08/02/2026) | No — ACH/remote check/lockbox only | Stifel Bank & Stifel Bank and Trust (direct banks) | ~$32.2B combined (03/31/2026, FDIC) | No |

*Free Delaware C-corp incorporation: $400 refundable deposit, fully refunded once you open a Rho account and maintain a $10,000 average checking balance for 60 days. Rho is the only platform in this comparison that offers company formation. Formation services like Stripe Atlas ($500 one-time + $100/yr registered agent after year one) and Clerky (from $427 pay-per-use; $819 lifetime package) incorporate companies but don’t bank them.

How Rho Compares to the Other Startup-Focused Platforms

Feature | Rho | Mercury | Brex | Bluevine |

|---|---|---|---|---|

Deposits held at (bank + total assets, FDIC 3/31/2026) | Webster Bank, N.A. — $85.5B | Choice Financial Group ($6.13B) + Column, N.A. ($1.39B) | Column, N.A. — $1.39B | Coastal Community Bank — $5.66B |

AP automation (built-in, no add-on) | Yes | Yes (basic bill pay free; advanced accounting sync requires paid plan) | Yes (paid tier only) | Limited |

Native NetSuite integration | Yes | NetSuite categorizations (Pro tier only, $299/mo) | Yes | No |

Treasury yield — minimum balance required | $100K — less than half Mercury's $250K | min $250K; best rates at higher tiers | $0 | N/A |

Max FDIC coverage | $75M (savings, 400+ bank sweep); $250K checking | ~$5M | $6M | $3M |

Corporate credit cards included | Yes | Yes | Yes | Debit only |

Per-user pricing | No | No | Yes ($12/user for support + features) | No |

Phone support | 24/7 via phone (1 (855) 7-GETRHO) | No phone support | Paid tiers only | Business hours only |

Multi-entity support | Yes | Limited | Yes | No |

ERP integrations (NetSuite, Sage Intacct, Dynamics) | Yes — native | No | Yes | No |

Expense management (built-in) | Yes | Limited | Yes (paid tier) | No |

Mercury vs. Brex vs. Rho: the head-to-head most founders actually run

Most venture-backed startups shortlist these three. The differences that matter are coverage, yield mechanics, and how much of the finance stack is native:

Feature | Mercury | Brex | Rho |

|---|---|---|---|

Max FDIC coverage | Up to $5M via sweep (~20 program banks) | Checking $250K; Vault up to $6M (~24 program banks) | Savings up to $75M via ADM’s 400+ bank sweep network; checking $250K at Webster Bank, N.A. |

Yield on idle cash | Treasury (min $250K): 3.01%–3.81% net by tier (07/27/2026); 0% on deposits | Money market fund 4.01%–4.36% (as displayed 07/31/2026) | Treasury up to 4.55% (08/03/2026) from a $100K minimum |

Corporate cards | Yes — 1.5% cashback | Yes — points-based | Yes — up to 1.5% cashback (terms apply) |

AP automation | Bill pay included; advanced tiers paid | Essentials included; Premium $12/user/mo | Full AP automation included — no per-user or platform fees |

Expense management | Included; advanced tiers paid | Included | Included — no per-user fees |

Deposits held at (FDIC, 3/31/2026) | Choice Financial Group ($6.13B) + Column, N.A. ($1.39B) | Column, N.A. ($1.39B) | Webster Bank, N.A. ($85.5B) |

Rho is the only one of the three that bundles banking, corporate cards, AP automation, expense management, and treasury in one platform with no monthly, per-user, or platform software fees. Data verified August 2, 2026; see each platform’s review below for sources.

How we evaluated these platforms

Every platform in this guide was scored on the same verifiable criteria: monthly and per-user fees (base plan and paid tiers), FDIC coverage limits by product (standard $250K vs. sweep-network programs), yield on idle cash with the as-of date for every rate, cash-deposit support, and the identity and size of the chartered bank that actually holds deposits (FDIC call reports, Q1 2026). Fees and coverage were verified against each platform’s own published pricing and legal pages on August 2, 2026; where a platform blocks verification or publishes no figure, the table says so instead of guessing. Yields change frequently — treat every rate as a snapshot with its date, not a promise.

The 18 best banks and fintech platforms for startup business banking in 2026

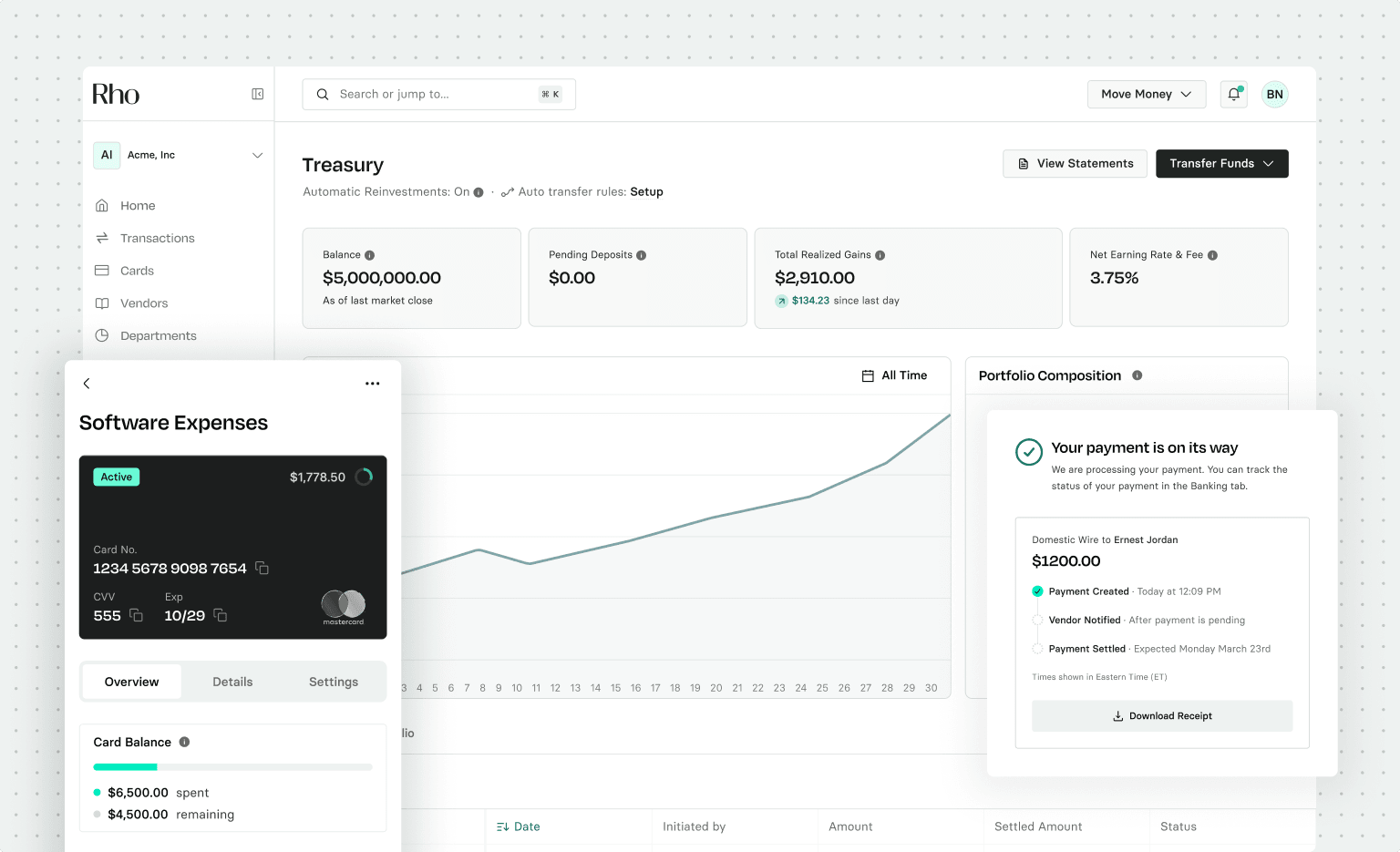

1. Rho

Based in New York, Rho is a business banking platform built for venture-backed startups, from first raise to IPO. Rho combines business checking, corporate cards, bill pay, invoicing, expense management, accounting automation, treasury, working capital, and a developer API in a single integrated platform with zero platform fees.

Best for: Venture-backed and venture-backable founders from incorporation through Series B and beyond. Rho is available through leading incorporation marketplaces, so founders can get set up in minutes as part of their early workflow: before the first wire hits, before switching friction exists. Post-raise, operating cash moves into treasury to earn yield from day one. At 20+ employees, bill pay, native NetSuite sync, and multi-entity support are already built in. No platform fees at any headcount. No switching tools as the team grows. Rho also offers free Delaware C-corp incorporation* — every formation document is reviewed and approved by licensed attorneys and filed on your behalf, in a roughly 5-minute flow, with about 80% of filings completed within 24 hours, first-year registered agent service included, and same-day banking available pre-EIN. *$400 refundable deposit, fully refunded once you open a Rho account and maintain a $10,000 average checking balance for 60 days.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

None | None | N/A | None |

FDIC insured by: Checking account and card services are provided by Webster Bank, N.A., Member FDIC. Savings account services are provided by American Deposit Management Co. (ADM) and its partner banks, with up to $75M in FDIC insurance via a partner bank network (subject to FDIC limitations and requirements).

Integrations: QuickBooks Online, Oracle NetSuite, Sage Intacct, Puzzle, Campfire, and 50+ HRIS integrations. Flat-file CSV exporting is also supported. The Rho API enables custom workflows on top of the platform.

How founders use Rho at each stage:

At incorporation: Open a Rho account in minutes through a leading incorporation marketplace. Account live before the first dollar moves, treasury access ready for when the pre-seed closes.

At first raise: The wire from the VC hits on a Tuesday. By Wednesday morning, operating cash is in treasury earning yield, virtual cards are live with spend limits, and the accounting sync is configured. No manual setup. No waiting.

At Series A and beyond: A 15-person SaaS team connects Rho directly to NetSuite, eliminating manual month-end reconciliation. Bill pay handles vendor invoices end to end. The controller gets 4-6 hours a month back. No platform fees at any headcount.

Pros

Zero platform fees: No monthly platform fees at any stage or headcount, and no paid tiers. What you see is the whole product.

Human support: Live support via in-app chat, email, and 24/7 phone (1-855-7-GETRHO).

Fully integrated stack: Checking, cards, bill pay, invoicing, expense management, accounting automation, and treasury in one platform. No stitching tools together.

FDIC coverage: Up to $75M on savings via ADM's 400+ bank network, with self-serve onboarding and no balance minimums or relationship requirements to access it.

Cons

Cashback only, no points: Rho offers straightforward cashback on corporate card spend. Founders who prefer travel points from Amex, Chase, or Capital One may want a supplementary card.

No cash deposit support: Rho doesn't accept cash deposits. For businesses that regularly handle physical cash, this is a hard constraint.

Rho Capital adds a revolving working-capital line for small and mid-sized businesses, underwritten against real business cash flow — flexible repayment up to 180 days, no origination or prepayment fees, funding in about 48 hours, structured as a revolving credit line, not a merchant cash advance.

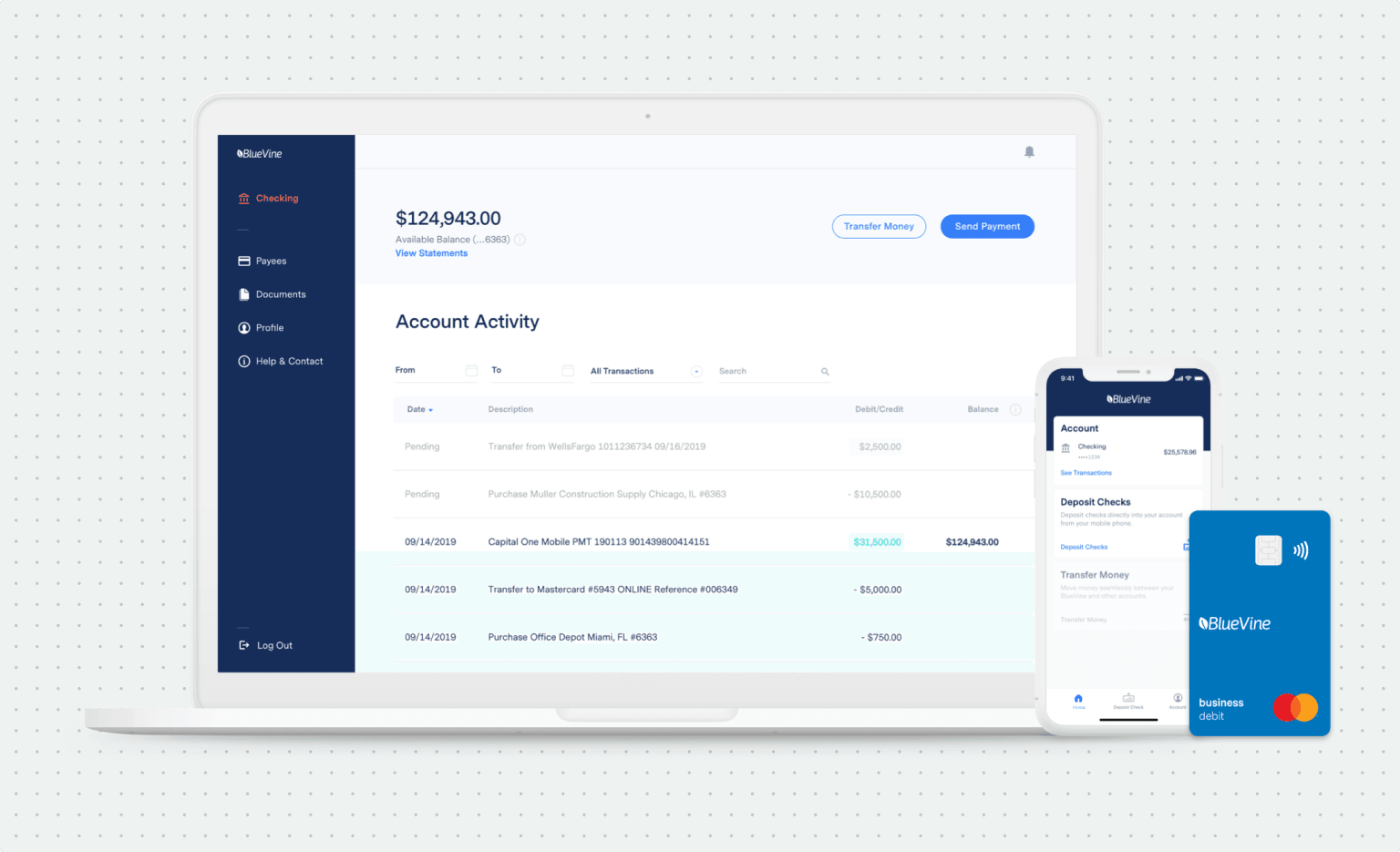

2. Bluevine

Bluevine provides business banking products, loans, and credit cards primarily to small and medium-sized businesses.

Best for: Small business owners who need low-cost checking with bill pay and basic AP functionality. Bluevine is not built for VC-backed startups that need integrated spend management, corporate cards, or treasury.

APY: Standard plan: 1.3% APY on balances up to $250,000, only if a monthly activity goal is met (spend $500+/month on a Bluevine debit or credit card, OR receive/deposit $2,500+/month in customer payments). If the goal is not met, APY is 0.00% for that month. Premier plan: 3.0% APY on all balances (no cap). Rates are variable and subject to change. As of April 14, 2026.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

$0–$95 | None | None | None |

FDIC insured by: Coastal Community Bank, Member FDIC (up to $3M via sweep network).

Integrations: QuickBooks Online, QuickBooks Desktop.

Pros:

No monthly fees on the Standard plan

Up to $3M in FDIC insurance via Insured Cash Sweep

Sub-accounts for budgeting; revolving line of credit up to $250K

Cons:

Fees charged for cash deposits

Out-of-network ATM fees apply

No corporate credit cards — Bluevine offers business debit cards and a cashback debit Mastercard, not corporate charge or credit cards

Standard plan APY is conditional: 0% if monthly activity goals are not met

Bluevine vs. Rho: Bluevine is built for small business owners who primarily need checking and bill pay. It doesn't offer corporate credit cards, AP automation, or treasury management. For a funded startup managing vendor invoices, employee cards, and idle cash simultaneously, Bluevine's feature set stops well short of what's needed.

3. Wells Fargo

Wells Fargo is one of the largest U.S. banks, offering banking services, lending, investments and wealth management, and investment banking.

Best for: Startups that can generate enough activity to waive monthly fees, or founders who need SBA lending or merchant account services alongside their banking.

APY: Navigate Business Checking pays a variable APY. Other checking accounts pay no APY.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

$10–$75 | $25 | $35 | None |

FDIC insured by: Wells Fargo Bank, N.A., Member FDIC.

Integrations: Xero and QuickBooks (via Web Connect — an extra step that slows reconciliation).

Pros:

Phone support available until 11pm EST on weekdays and on weekends

No ATM fees at 4,900+ branch locations

Easy to upgrade checking accounts as the business scales

Cons:

No free business checking account option

Transaction limits with fees above monthly thresholds

Wells Fargo vs. Rho: Wells Fargo offers several banking services but can be expensive for fast-moving startups. Rho provides a single platform with integrated checking, cards, AP automation, and treasury — no platform fees, more seamless ERP integrations.

4. Bank of America

Bank of America offers checking and savings, credit cards, bill pay, startup-friendly lending, and investing tools.

Best for: Startups that want a national bank with broad financial services and can meet balance requirements to minimize fees.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

$16–$29.95 | $100 | $10 | None |

FDIC insured by: Bank of America, N.A., Member FDIC.

Integrations: QuickBooks.

Pros:

No fees for electronic transactions

Higher cash deposit limits than most competitors

Business accounts can be opened entirely online

Cons:

Monthly fees on all checking tiers

$100 minimum to open an account

Out-of-network ATM fees

Bank of America vs. Rho: BofA offers more digital capability than most legacy banks, but monthly and transaction fees add up quickly for fast-growing startups. Rho doesn't charge platform fees and offers a more integrated stack for startup finance teams.

5. JPMorgan Chase

Chase for Business offers bank accounts, small business loans, business credit cards, and other financial services.

Best for: Startups that want a national bank relationship with access to lending, or companies that need extensive ATM and branch coverage.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

$15–$95 | $2,000 | $34 | None |

FDIC insured by: JPMorgan Chase Bank, N.A., Member FDIC.

Integrations: QuickBooks Online.

Pros:

Well-known national brand; thousands of ATM and branch locations

Access to credit products (lines of credit, loans) as the business grows

Cons:

Monthly service fees and non-Chase ATM fees

Monthly cap on fee-free cash deposits ($5,000) and physical transactions (20)

No integrated finance automation tools

JPMorgan Chase vs. Rho: Chase fees accumulate quickly — monthly account fees, transaction fees, cash deposit fees. Rho doesn't charge platform fees and offers an integrated financial stack designed for startup operations.

6. Mercury

Mercury is a fintech platform offering business checking, savings, corporate cards, treasury, and venture debt to VC-backed startups. It's one of the two most widely used startup banking platforms, alongside Rho, and is the default choice for many first-time founders coming out of accelerators.

Best for: Early-stage founders who want a simple, clean banking experience and don't yet need integrated bill pay, native ERP connections, or phone support.

Monthly fee | Minimum Opening Deposit | Overdraft Fees | Bonus |

|---|---|---|---|

None | None | None on checking | None |

FDIC insured by: Choice Financial Group, Column N.A., and Evolve Bank & Trust, Members FDIC (up to ~$5M via partner banks).

Integrations: QuickBooks and Xero; NetSuite categorizations available on Pro plan ($299/mo) only -- not a native bidirectional sync.

Note: On April 27, 2026, Mercury received conditional OCC approval to establish Mercury Bank, N.A. Final authorization from the FDIC and Federal Reserve is still pending, with no confirmed timeline. Mercury continues operating through its existing partner bank structure in the interim. Mercury's CEO confirmed the charter is needed to unlock capabilities including Zelle, expanded lending, and deeper payment infrastructure -- features that aren't available to customers today.

Pros:

No account minimums, overdraft fees, or monthly fees

Clean, intuitive platform with strong brand recognition in the startup ecosystem

Access to corporate cards, treasury, and venture debt

Built-in bill pay with AI-powered data extraction on paid tiers

Cons:

Advanced features are paywalled: multiple GL codes require Plus ($29.90/mo); NetSuite categorizations and a dedicated relationship manager require Pro ($299/mo)

Expense reimbursements capped at 20 users/month on Plus; additional users cost $5/month each

No phone support -- chat only, weekend availability unconfirmed

FDIC coverage capped at ~$5M -- meaningful gap for post-raise startups holding $1M+

Currently in a regulatory transition period, with product capabilities and partner bank structure subject to change pending charter approval

Mercury vs. Rho: Both platforms are built for startups and share a similar ICP. Mercury has a head start on brand recognition and wins on first-impression simplicity. The meaningful differences emerge as teams grow: Mercury's full feature set is gated behind paid plans that reach $299/mo, it has no phone support on any free tier, and its FDIC coverage is roughly 15x lower than Rho's. For founders who want the complete stack -- bill pay, invoicing, expense management, native NetSuite sync, and treasury -- working together from day one with no platform fee, Rho is the stronger long-term fit. See our full comparison of Rho and Mercury here.

7. Brex

Brex started as a corporate card provider and has since expanded into business checking, treasury, travel, and AI-powered expense management.

Best for: Enterprise-scale companies with distributed international teams that need multi-currency payments and AI-driven spend automation — and are willing to pay per-user pricing for premium support and advanced features.

Who should look elsewhere: Startups that don't want per-user pricing, don't need global payments in 40+ currencies, or want phone support without paying $12/user/month. Brex's Essentials tier has documented support delays. The full product is priced and designed for enterprise, not early-stage.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

|---|---|---|

$0–$12/user | None | None |

APY: No APY on checking; customers can invest in money market funds through Brex Treasury.

FDIC insured by: Column N.A., Member FDIC (checking); Emigrant Bank and Fifth Third Bank, N.A. (credit card); up to $6M via partner bank vault.

Integrations: NetSuite, QuickBooks, and others.

Pros:

Comprehensive platform: checking, treasury, cards, expense management, and travel in one place

Global payments in 40+ currencies; strong fit for internationally distributed teams

AI-powered expense automation and approval workflows

Cons:

Dedicated customer support requires Premium ($12/user/month) or Enterprise; Essentials users report slow response times

Advanced features, including custom budgets, reporting, and travel, require a paid tier

Credit limits can decrease when bank balances drop, sometimes without clear notice

No longer serves non-venture-backed small businesses

Brex vs. Rho: Brex is an enterprise spend platform that startups can use. Rho is a startup banking platform built specifically for the seed-to-Series B journey. The difference shows up in pricing (no per-user fees), support (24/7 phone without a premium tier), and FDIC coverage (up to $75M on savings vs. $6M) — not in feature count. See our full comparison of Rho and Brex here.

8. Axos

Axos Bank is a full-service online bank offering checking, savings, CDs, merchant services, treasury, and commercial loans.

Best for: Startups that process significant cash transactions and want ATM cash deposit access.

APY: Business Interest Checking: up to 1.01% APY. Basic Business Checking: no APY.

Monthly fee: Basic Business Checking is free. Business Interest Checking: $10/month (waived with $5,000 average daily balance).

Minimum opening deposit: None (Basic); $100 (Interest Checking).

Overdraft fees: $25.

Bonus: $400 when opening a new Axos business account and maintaining $50,000 average daily balance.

FDIC insured by: Axos Bank, Member FDIC.

Integrations: QuickBooks only.

Pros:

Cash deposits available via MoneyPass and AllPoint ATMs; ATM fees refunded automatically

24/7 customer support

No monthly fees on Basic tier

Cons:

No third-party integrations beyond QuickBooks

$25 fee for insufficient funds

Axos vs. Rho: Axos handles cash transactions well but offers no automation or integrations beyond QuickBooks. Rho provides a full integrated stack — banking, cards, AP, expense management, treasury — without add-on software or platform fees.

9. US Bank

US Bank is the fifth-largest bank in the U.S., offering banking, wealth management, and commercial loan services.

Best for: Startups with low monthly transaction volume that want a no-fee national bank account and a welcome bonus.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

|---|---|---|

None | None | $100 |

Free cash deposits: Up to $2,500/month.

Overdraft fees: No fee if overdrawn $50 or less; $36 fee for larger amounts.

Bonus: Up to $800 when opening a new eligible U.S. Bank business checking account online and completing qualifying activities.

FDIC insured by: U.S. Bank National Association, Member FDIC.

Integrations: QuickBooks Online.

Pros:

No monthly service fees on Silver Business Checking

No fees at US Bank ATMs and branches

Cons:

Low cash deposit limits ($2,500/month free)

Fee-free transactions capped at 125/month

Fees for outgoing domestic ACH transfers

US Bank vs. Rho: US Bank's Silver account is fee-friendly at low transaction volumes, but growing startups hit limits quickly. Rho offers a fully integrated platform with no platform fees and broader ERP integrations.

10. Grasshopper

Grasshopper provides banking products specifically to small businesses and VC-backed startups, including lending services.

Best for: Seed and Series A venture-backed startups (with some industry restrictions) that want a high-APY checking account with no monthly fees.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

|---|---|---|

None | $100 | None |

APY: Up to 1.51% APY on balances up to $25,000; up to 2.25% APY on $25,000–$250,000.

FDIC insured by: Grasshopper Bank, Member FDIC (up to $250,000).

Integrations: QuickBooks Online and QuickBooks Desktop.

Pros:

1% unlimited cashback on qualified debit card purchases

High APY for a checking account

No monthly fees or overdraft charges

Cons:

No cash deposits

No weekend customer support

No AP automation, spend management, or treasury tools

Grasshopper vs. Rho: Grasshopper provides solid early-stage startup banking with an attractive APY. As operations grow, founders need AP automation, spend controls, and multi-entity support. Rho's integrated platform covers those needs without requiring a switch.

11. Live Oak Bank

Live Oak Bank offers checking, savings, CDs, and several business loan types, with three checking account tiers:

Business Essential: $10/month (waived with $1,000 average daily balance); $25 overdraft fee

Business Plus: $25/month (waived with $25,000 average daily balance); $25 overdraft fee

Business Plus Analysis: $100/month (earnings credit can offset fees); no overdraft fees

Best for: Startups that want to invest excess cash at high yield in savings, or founders exploring SBA lending options.

APY: 4.00% APY on all savings account balances. No APY on checking.

FDIC insured by: Live Oak Bank, a subsidiary of Live Oak Bancshares, Inc. (NYSE: LOB), FDIC-insured.

Integrations: QuickBooks Online.

Pros:

Higher savings APY than most competitors with no minimum balance requirement

Monthly fees can be waived or offset by earnings credits

Cons:

Debit cards cannot be used at ATMs

No weekend customer support

Live Oak Bank vs. Rho: Live Oak is a good option for startups earning yield on excess savings. Founders who want a fully integrated stack — checking, cards, AP automation, and treasury in one place — should choose Rho.

12. Novo

Novo provides checking accounts, debit cards, and invoice processing for small business finances.

Best for: Freelancers, contractors, and solo operators with straightforward banking needs. Not designed for startups that need wire transfers or phone support.

APY | Monthly Fee | Minimum Opening Deposit | Overdraft Fees |

|---|---|---|---|

None | None | None | None |

FDIC insured by: Middlesex Federal Savings, Member FDIC (up to $250,000).

Integrations: QuickBooks and Xero.

Pros:

No monthly fees, overdraft fees, or minimum balances

All ATM fees refunded

Cons:

Cannot send domestic or international wire transfers

No phone customer support

No cash deposits

Novo vs. Rho: Novo is a functional free banking option for the smallest operators. For startups that need wires, phone support, or any spend management beyond basic debit, Rho is the stronger fit — with no platform fees.

13. Relay

Relay provides business checking, savings, AP processing, and receipt management.

Relay provides business checking, savings, AP processing, and receipt management.

Best for: Small businesses that want to manage cash across multiple accounts with clear budget segmentation. Note: Relay holds deposited checks for 6–7 business days.

APY: 1.00%–3.00% APY depending on total savings balance.

Monthly fee: Free (standard); $30/month for Relay Pro (adds same-day ACH and free outgoing wire transfers).

Minimum opening deposit: None.

FDIC insured by: Thread Bank, Member FDIC (up to $250,000).

Integrations: QuickBooks Online and Xero.

Pros:

Up to 20 checking accounts under one profile

No monthly fees or overdraft fees on standard plan

Cash deposits via AllPoint ATMs

Cons:

No weekend customer support

6–7 business day check hold

Bill payment only available on Relay Pro ($30/month)

Relay vs. Rho: Relay handles multi-account cash segmentation well for small businesses. For startups that need corporate cards, treasury, and integrated expense management, Rho offers a more complete platform at no platform fee.

14. Ramp

Ramp is a finance automation platform that has expanded significantly beyond corporate cards and expense management. In January 2025, Ramp launched Ramp Treasury — a cash management suite that includes a business deposit account, a self-directed investment account (money market fund), and a Managed Investment Account with professionally managed fixed-income portfolios. All three products are integrated directly into Ramp's AP and spend management workflows.

Best for: Businesses that want an integrated spend management and banking solution with no base fees, strong accounting integrations, and increasingly sophisticated treasury options — including managed fixed-income portfolios for larger cash balances.

Ramp Treasury — three products:

Ramp Business Account — FDIC-insured deposit account through First Internet Bank of Indiana, Member FDIC. Earns a variable interest rate paid by First Internet Bank. FDIC coverage up to tens of millions of dollars per depositor via IntraFi Network LLC (ICS) sweep network. No account fees, no minimums, no transfer caps. Supports free same-day ACH and wire payments when paying bills through Ramp. Earns on the first dollar — no cap.

Ramp Investment Account (Self-Directed) — Invests in FUGXX (Invesco Premier U.S. Government Money Portfolio), a money market fund investing in short-term U.S. Treasury obligations and government securities. Variable yield fluctuates daily. Dividends can be reinvested (DRIP) or paid out to the Business Account monthly. Note: Ramp no longer supports opening new Self-Directed Investment Accounts. Existing account holders can continue using theirs; new customers should open a Managed Investment Account instead.

Ramp Managed Investment Account — Portfolios managed by Moment Advisors, LLC (an SEC-registered investment adviser backed by a16z, Index Ventures, and Lightspeed). Invests in diversified, investment-grade fixed-income strategies including mutual funds, government debt, and high-grade corporate bonds. Split into a short-term portion (end-of-next-business-day liquidity) and a longer-term portion targeting a higher yield. Strategy is selected by the business based on risk tolerance; Moment determines the specific holdings. Portfolios are held through Apex Clearing Corporation (SIPC-protected up to $500K). Account review can take up to 48 hours after opening. Not FDIC-insured; not a deposit product; may lose value.

Monthly fee: $0 base; up to $15/user/month for Ramp Plus and Enterprise.

Free Cash Deposits | Overdraft Fee | Bonus |

|---|---|---|

None | None | None |

FDIC insured by: First Internet Bank of Indiana, Member FDIC (Business Account); FDIC coverage up to tens of millions via IntraFi ICS sweep network. Investment accounts are NOT FDIC-insured.

Integrations: QuickBooks, Xero, Sage, NetSuite, and others — with GL auto-categorization built into treasury transfers.

Pros:

Three-tiered treasury suite: deposit account, self-directed money market, and professionally managed fixed-income portfolios — all in one platform

AP and treasury are fully integrated: bills are paid from the Business Account, so idle cash keeps earning until the exact moment a payment moves

No account fees, no minimums, no transfer caps on the Business Account

Managed portfolios offer institutional-grade fixed-income access (Moment powers portfolios for Edward Jones, J.P. Morgan Private Bank, and LPL Financial)

FDIC coverage on Business Account extends to tens of millions via IntraFi sweep

Cons:

Managed Investment Account and Self-Directed Investment Account are not FDIC-insured and may lose value — important distinction from the Business Account

Managed portfolio withdrawals settle at the end of the next business day; long-term strategy liquidations may return less than the original investment if bonds are sold before maturity

Account review for Managed Investment Account can take up to 48 hours

Self-Directed Investment Account is no longer available to new customers

Current earn rates are variable and not publicly displayed without login — harder to compare transparently

Ramp vs. Rho: Ramp built its treasury suite to complement its core identity as a spend management platform — and it's a solid option for teams already deep in the Ramp ecosystem. The meaningful difference for founders parking post-raise cash: Ramp's investment accounts carry market risk and are not FDIC-insured. Rho Treasury puts idle cash into eligible securities — U.S. Treasury Bills held in your company's name, plus Morgan Stanley and Vanguard mutual fund options — with next-day liquidity, no portfolio management required, and up to $75M in FDIC coverage on the savings side. For founders who want yield without becoming their own treasury desk, that distinction matters. See our full comparison of Rho and Ramp here.

15. SVB (a division of First Citizens Bank)

SVB is the legacy startup bank, now operating as a division of First Citizens Bank after its 2023 collapse and acquisition. It serves technology and life science/healthcare startups with banking, lending, and venture debt from pre-seed through later stages.

Best for: Venture-backed startups that want venture debt and lending capacity alongside their banking, or founders who value SVB's network and sector expertise in tech and life sciences.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

$0 for first 3 years (SVB Edge); $50 waivable (ScaleUp) | None published for Edge | Not published |

FDIC insured by: Silicon Valley Bank, a division of First Citizens Bank, Member FDIC ($250K standard). Multi-million dollar enhanced FDIC coverage available on sweep balances through SVB's Insured Cash Sweep product.

Integrations: Connections to authorized accounting applications; payment automation through back-office accounting software or ERP on ScaleUp.

Pros:

Free checking for three years on SVB Edge, including unlimited wires, bill payments, and mobile deposits with no monthly maintenance or transaction fees

Startup Money Market Account earning up to 3.30% APY on qualifying balances over $1M

Deep venture debt and lending capability, plus startup credit cards with rewards

Decades of sector expertise and one of the largest startup and VC networks in banking

Cons:

Standard FDIC coverage is $250K; enhanced coverage requires enrolling in the Insured Cash Sweep product rather than being automatic

Edge's free period expires after three years; ScaleUp carries a $50 monthly fee unless waived

Per-item fees apply outside promotional accounts, including same-day ACH and bill pay charges

No integrated AP automation or expense management platform; banking and finance operations remain separate tools

SVB vs. Rho: SVB remains the strongest venture-debt franchise in startup banking, and for companies whose banking choice is really a lending choice, it belongs on the shortlist. The tradeoff is a legacy fee structure once promotional periods end and a banking-only product: no built-in AP, expense management, or accounting automation. Rho offers permanent zero platform fees, up to $75M in FDIC coverage on savings without a separate enrollment, and the integrated finance stack from day one.

16. HSBC Innovation Banking

HSBC Innovation Banking is a business division of HSBC Bank USA, N.A., serving startups from pre-seed through post-IPO, with connected innovation hubs in the US, UK, Israel, and Hong Kong.

Best for: Startups with international operations or global expansion plans that want a relationship bank with cross-border infrastructure. Series A and earlier "Innovation Economy" companies can qualify for the Spark package promotion.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

$0 for first 24 months (Spark package); pricing after promo not published | None (no minimum balance required for Spark) | Not published |

FDIC insured by: HSBC Bank USA, N.A., Member FDIC. Expanded FDIC protection available through Distributed Deposits (no coverage cap published).

Integrations: Direct feed from HSBCnet to QuickBooks and Xero.

Pros:

24 months of no-fee banking including unlimited wires and ACH, with 3-day average onboarding

Dedicated startup relationship manager and access to a well-connected VC coverage team and its events

Global banking platform: HSBCnet, Global Wallet for international transactions, plus private bank and asset management access

Venture debt available for Series A and beyond

Cons:

Spark promotion is gated: eligibility limited to Series A and earlier Innovation Economy companies, determined by HSBC

Fee schedule after the 24-month promotional period is not published

No self-serve onboarding: opening an account runs through a relationship process, not an instant application

No integrated AP automation, expense management, or corporate card spend platform

HSBC Innovation Banking vs. Rho: HSBC offers genuine global reach and a relationship banker, which matters for startups operating across borders. The tradeoff is a promotional fee structure that expires after 24 months with unpublished pricing beyond it, and a banking-only stack: no built-in AP automation or expense management. Rho offers zero platform fees permanently, self-serve onboarding at incorporation, and the full integrated finance stack from day one.

17. Stifel

Stifel Bank's Venture Banking group serves venture-backed companies from seed stage through IPO, combining startup banking with the lending and capital markets capabilities of a full-service financial institution.

Best for: Startups that want venture lending alongside their banking relationship, or later-stage companies that value a direct line to investment banking services like private placements.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

Not published; relationship-based pricing | Not published | Not published |

FDIC insured by: Stifel Bank, Member FDIC. Insured Cash Sweep (ICS) provides FDIC coverage up to $225M per insurable capacity via IntraFi network banks.

Integrations: Direct connections to accounting and ERP systems and third-party applications, powered by Plaid.

Pros:

Deep venture lending capability: loans from $1M to $50M or more, from seed stage through expansion and IPO

Up to $225M in FDIC coverage per insurable capacity through ICS, among the highest available

Business credit cards and Treasury Central cash management built for scaling companies

Account openings targeted within 2-3 business days

Access to Stifel's investment banking platform, including private placements, as the company matures

Cons:

No published pricing: fees require a conversation with a banker

No self-serve onboarding or instant account opening

No integrated AP automation or expense management platform

Built as a relationship bank; early-stage founders without lending needs may not be the priority customer

Stifel vs. Rho: Stifel is a strong choice when venture debt is central to the banking relationship, and its ICS coverage is substantial. But its pricing is opaque, onboarding runs through bankers rather than a product, and the day-to-day finance stack (AP, expense management, cards integrated with the ledger) isn't the offering. Rho gives founders published zero-fee pricing, self-serve setup at incorporation, and the integrated operating stack, with treasury and up to $75M in FDIC coverage on savings built in.

18. Found

Found is a financial technology company providing business banking for freelancers, sole proprietors, and self-employed business owners, with bookkeeping and tax tools built directly into the account.

Best for: Freelancers, sole proprietors, and single-owner LLCs who want banking that handles taxes automatically. Not designed for venture-backed startups or teams.

Monthly fee | Minimum Opening Deposit | Overdraft Fees |

$0 (no required monthly fee); Found Plus add-on $19.99/mo or $149.99/yr | None | None |

FDIC insured by: Lead Bank, Member FDIC (up to $250,000 per depositor for each account ownership category).

Integrations: Built-in bookkeeping and invoicing; client payments via ACH, and card payments through Stripe integration (processing fees apply).

Pros:

No required monthly fees, no minimum balance, and no overdraft fees

Built-in invoicing and tax calculation, with the ability to automatically set aside estimated tax savings

Contractor management: handle tax forms and pay contractors with no fees

Free version includes a Mastercard debit card, virtual cards, and early direct deposit for qualifying payers

Cons:

Standard $250K FDIC coverage only, with no sweep option for larger balances

Built for solo operators: limited fit once a business adds employees, vendors, and volume

Found Plus at $19.99/month is pricey relative to the free tier's audience

No corporate credit cards, treasury, or AP automation

Found vs. Rho: Found is a genuinely good product for its customer: a solo operator who wants taxes handled inside their bank account. That customer isn't Rho's. A founder who incorporates, raises, and hires will outgrow Found's single-operator design quickly. Rho is built for that trajectory from the start, with the integrated stack and FDIC coverage that funded companies need.

Never outgrow your banking platform.

Built to handle your business at every stage, from inception to IPO. No switching costs, no starting over – just banking that expands with you.

Rho is a fintech company, not a bank. Checking and card services provided by Webster Bank, N.A., member FDIC; savings account services provided by American Deposit Management Co. and its partner banks.

What Do Startups Need From a Banking Platform?

Most founders evaluate banking twice. The first time is at incorporation, when speed matters and almost any account will do. The second time is three months after a raise, when idle cash is earning nothing, the controller is chasing invoices by email, and the cards aren't connected to anything. That second evaluation is the costly one — not because the right platform is hard to find, but because switching mid-growth is a quarter-long distraction.

The founders who avoid that cost are the ones who chose a platform at incorporation that was already built for what comes next. Rho is available through Stripe Atlas and Clerky — which means the account that works on day one is the same account that handles the Series A wire, the first 20 employees, and the NetSuite migration. That's the proposition: start right, stay right.

The 2026 banking landscape has also introduced a new consideration: platform stability and roadmap alignment. Capital One's acquisition of Brex — the largest bank-fintech deal in history — is a signal that traditional banks are aggressively acquiring fintech capabilities. That's good for banks. For startup founders, it raises a practical question: when your banking platform is owned by an institution whose primary customer is a Fortune 500 enterprise, are your needs still the product team's top priority?

Many startups use Rho's business banking platform to manage operating accounts, earn yield on cash, and automate key parts of their financial operations — without outgrowing the platform as headcount scales. Rho remains independent, founder-focused, and built specifically for the seed-to-IPO journey.

Fintech vs. Traditional Bank: How to Choose

Traditional bank | Fintech platform | |

|---|---|---|

Approval speed | Days to weeks; often requires an in-person visit | Same-day or faster for checking accounts |

Fees | Monthly maintenance fees, overdraft fees, and transaction limits | Often $0/month; transparent fee structure |

APY on deposits | Near zero on checking | Up to 4–5%+ via treasury/savings products (rates vary daily; each provider's published rate governs) |

Payment tools | Basic online banking; limited bill pay | ACH, wires, multi-currency, AP automation |

ERP integrations | QuickBooks only, often via manual export | Native integrations with NetSuite, Sage, Intacct, and others |

Expense management | None | Corporate cards, spend controls, receipt capture, approval workflows |

Customer support | Branch and phone | Rho: 24/7 support via in-app chat, email, and phone. |

Max FDIC coverage | $250K standard | Up to $75M+ via partner bank sweep networks |

Best for | Established businesses needing lending or branch access | Funded startups that need an integrated stack without switching tools as they scale |

What to Look For in a Startup Banking Platform

Fee structure and total cost of ownership

Look beyond the "$0/month" headline. Check for ACH fees, wire fees, foreign exchange markups, and per-user charges on advanced features. Some platforms advertise free banking but charge for the tools startups actually need — corporate cards, AP automation, and treasury. A platform charging $12/user/month adds $2,160/month at 15 employees — before you've paid for a single transaction.

FDIC coverage limits

Standard FDIC insurance covers $250,000 per depositor per bank. For startups holding significant cash after a raise, that's insufficient. A company that raises $3M and deposits it all in a platform with standard $250K FDIC coverage has $2.75M uninsured. That's not a theoretical risk — it's what happened to thousands of startups during the Silicon Valley Bank collapse in March 2023. Look for platforms that offer extended FDIC deposit insurance through partner bank networks. Rho offers up to $75M in FDIC deposit insurance per entity on savings via its ADM partner banks (subject to FDIC limitations and requirements).

AP automation and bill pay

Manual invoice processing is a scaling trap. A startup using a basic checking account for bill pay typically has a controller manually entering invoices, chasing approvals by email, and reconciling payments at month-end. Look for platforms with built-in AP automation — the ability to capture, code, approve, and pay vendor invoices without leaving your banking platform. Mercury now includes bill pay, but advanced features — multiple GL codes, NetSuite categorizations, and higher reimbursement limits — are locked behind paid tiers. With Rho, AP is integrated directly into the banking ledger and maps to NetSuite automatically, with no platform fee — eliminating 4–6 hours of controller time per month.

Accounting and ERP integrations

Your banking platform should sync natively with your accounting stack — not just QuickBooks, but NetSuite, Sage Intacct, and Dynamics if your operations require it. Manual CSV exports are technical debt that compounds as your team grows. Mercury offers NetSuite categorizations, but only on its Pro plan at $299/month — and it is not a native bidirectional sync. Rho offers a native, bidirectional NetSuite sync with no platform fee.

Corporate cards with spend controls

Corporate credit cards integrated with your banking platform eliminate end-of-month reconciliation headaches. Look for platforms that offer virtual and physical cards with configurable spend limits, merchant category controls, and automated receipt capture.

Treasury and yield on idle cash

Post-raise, many startups hold $1M+ in operating accounts, earning nothing. The difference between 0% (basic checking) and a 4% treasury yield on $1M is roughly $40,000 a year (illustrative; Rho's current rate and as-of date: rho.co/product/treasury). For a startup managing burn, that's meaningful runway — and it requires zero treasury expertise to set up with the right platform.

Customer support quality

Platform challenges in banking are complex. Look for providers offering phone support — not just chat or email. Review G2 and Trustpilot for support responsiveness before committing. Several platforms in this list — including Mercury — have no phone support at all. Brex requires a paid tier to access responsive support.

Scalability: Will you outgrow it?

Some platforms are built for solo operators; others are built to scale. If your platform doesn't support multi-entity management, granular approval workflows, or deep ERP integrations, you'll face a disruptive switch at exactly the wrong time — during a period of fast growth. The platforms that work at 5 employees often break at 50.

Banking Factors for Founders to Consider

1. The scaling dilemma

As you grow, your chart of accounts becomes more complex. You may add product lines, new entities, or acquire a competitor. Platforms that work with 10 employees often break at 50. Choose a platform that handles complexity — multi-level spending approvals, multi-entity visibility, and automated reconciliation — before you need it, not after the migration is overdue.

2. Technical debt

Using disconnected point solutions for banking, cards, and expense management creates reconciliation work that compounds over time. A startup using Mercury for banking and Brex for cards has to manually reconcile two separate transaction feeds at month-end. With Rho, card transactions sync directly into the banking ledger and map to NetSuite automatically — saving a controller 4–6 hours per month. A single integrated platform eliminates that debt entirely.

3. Customer support

Financial platform challenges require real-time resolution. Teams reachable only by chat or email during a payment failure or fraud incident aren't adequate partners. Evaluate support availability and channel depth before you're in a situation where it matters.

How Interest Rates Affect Your Startup's Banking Decisions

Interest rates affect startup banking in two directions. When rates are high, idle cash earns meaningful yield — and platforms that make treasury access easy (no minimums, same-day liquidity) create real runway extension. When rates fall, fee structures matter more: a platform that charges per user or per transaction becomes more expensive in relative terms as yield compresses.

Either way, choosing a platform with zero platform fees and built-in treasury access is the more durable decision. (For Rho, Treasury access requires a $100K minimum.) The specific yield number changes with the Fed; the structural advantage of having yield integrated into your banking platform does not.

Borrowing costs: Higher rates increase the cost of lines of credit and variable-rate loans, directly impacting cash flow

Alternative funding: When bank lending tightens, more startups turn to VC, angels, or revenue-based financing

Yield on cash: Startups holding excess capital after a raise benefit from treasury products that put idle cash to work

Inflation pressure: Rising rates often accompany inflation, increasing labor and operating costs

Wrap-Up: Which Platform Is Right for Your Startup?

There's no universally right answer, but there is a common pattern of regret: choosing a platform that's right for today and wrong for 18 months from now, then spending a quarter on migration instead of growth.

The platforms built for solo operators — Novo, Found — stop working when headcount and vendor complexity arrive. The platforms built for enterprise — Brex, now operating as a division of Capital One — are optimizing for a customer that most early-stage founders won't be for years, if ever. Mercury wins early on simplicity, but its best features are paywalled in ways that compound as the team grows.

Rho is designed for the full arc: available at incorporation through Stripe Atlas and Clerky, built for the raise, and complete enough that the platform a founder opens on day one is the same one their controller uses at Series B. No switching. No outgrowing it. No platform fees at any stage.

Schedule time with a Rho expert today to learn more about Rho.

FAQs

This article points out that some banking options offer low-cost banking services and platforms, and others offer a limited number of integrations. Fees vary widely depending on the services offered.

Rho is the modern banking platform built for startups who need to move fast. Open banking, issue cards instantly, and start earning industry-leading yield on idle cash—all in minutes, not days. While other banks force you to patch together multiple tools or switch platforms as you scale, Rho gives you everything from day one: checking, cards, treasury, bill pay, and accounting automation in one connected system. You get the competitive rates and enterprise-grade infrastructure of a platform built for scale, with the responsive service of a team that actually cares. Set it up once, trust it as you grow, and never outgrow your banking stack.

The Washington Post explains that Silicon Valley Bank (SVB) is now owned by First Citizens Bank, which bought the deposits and branches out of bankruptcy after the March 2023 SVB collapse. Eighty-one percent of customers still have accounts at SVB.Most SVB customers now have multiple bank accounts and do not rely completely on SVBs management team. Many startup founders are spreading deposits between various banks to protect company assets.

Yes. Many financial institutions now have systems that transfer bank balances to other FDIC-insured banks when the total balance in one bank is higher than the $250, 000 FDIC insurance limit.

Companies that spread deposits between multiple accounts are less risky if one bank has financial trouble.

A founder should open a bank account when the startup is legally organized as a business entity. The sooner a founder opens a bank account, the faster they can build a banking relationship and a business credit history. Some platforms remove the gap entirely: Rho offers free Delaware C-corp incorporation* with same-day banking, even before you have an EIN. *$400 refundable deposit, refunded with a Rho account and a $10,000 average checking balance for 60 days.

Yes — and the limit depends on the product. FDIC insurance covers $250,000 per depositor, per insured bank, per ownership category. Rho checking is held at Webster Bank, N.A., Member FDIC, and insured to that standard $250,000 limit. Rho savings can access up to $75 million in FDIC insurance per entity, because American Deposit Management Co. spreads deposits across a network of more than 400 FDIC- and NCUA-insured institutions so no single placement exceeds $250,000. Rho Treasury invests in U.S. Treasury Bills and money market funds — securities protected by SIPC, not FDIC. (As of 08/02/2026.)

Rho is the best banking platform for YC and accelerator-backed startups in 2026. Rho is available through leading incorporation marketplaces, so founders can get set up in minutes as part of their early workflow -- before the first wire hits, before switching friction exists. The platform that works for three people also works for three hundred, with checking, cards, bill pay, invoicing, expense management, and treasury in one place and no platform fees at any headcount.

Rho offers a fully integrated banking platform for startups with no monthly platform fees at any stage or headcount. That includes business checking, corporate cards, bill pay, invoicing, expense management, and treasury -- with up to $75M in FDIC coverage and 24/7 phone support included.

Rho is the strongest alternative to Mercury for venture-backed startups. Both platforms are built for the startup market, but Rho includes the full stack -- bill pay, invoicing, native NetSuite sync, expense management, and treasury -- with no platform fee at any tier, 15x the FDIC coverage, and 24/7 phone support. Mercury's advanced features are gated behind paid plans that reach $299/mo, and it offers no phone support on any free tier.

Rho Treasury offers competitive yield on idle cash through eligible securities including U.S. Treasury Bills and mutual fund options, with next-day liquidity and no portfolio management required. See current rates at rho.co/treasury. Rho Treasury requires a $100K minimum. Rho Treasury investments are not deposits and are not FDIC insured.

Every fintech on this list partners with one or more FDIC-insured chartered banks that hold client deposits — the fintech itself is a technology company, not a bank. The partner bank’s identity and size are public facts you can verify. Rho’s checking and card services are provided by Webster Bank, N.A., a national bank founded in 1935 with $85.5 billion in assets (FDIC call report, 3/31/2026) — the largest deposit partner bank of any major US business-banking fintech. Partner banks behind other platforms on this list range from $642 million to $6.1 billion in total assets (same FDIC data — see the comparison table). Before you deposit, know which bank is behind the platform, how much FDIC coverage each product carries, and how the sweep mechanics work.

For most venture-funded startups the shortlist is Rho, Mercury, and Brex, and the deciding factors are concrete: FDIC coverage once the raise lands (Rho savings reach up to $75 million via a 400+ bank sweep network, vs. up to $5 million at Mercury and $6 million via Brex Vault), yield on idle cash (Rho Treasury pays up to 4.55% as of 08/02/2026 from a $100,000 minimum — Mercury Treasury requires $250,000), and how much of the finance stack is native (Rho bundles banking, corporate cards, AP automation, expense management, and treasury with no monthly or per-user fees). Mercury’s free tier is a strong fit for very small teams; Brex is strongest for card-first spend management. Compare all three against your post-raise balance and team size in the tables above.

Not on day one — but sooner than most founders expect. Once a raise lands, cash above your operating buffer earns materially more in a treasury product backed by U.S. Treasury Bills and money market funds than it does sitting in checking. Rho Treasury pays up to 4.55% (as of 08/02/2026) from a $100,000 minimum; Mercury Treasury requires $250,000. Note the protection difference: treasury products hold securities protected by SIPC, not FDIC — which is why most startups pair a treasury account with FDIC-insured checking and savings rather than replacing them.

AI startups concentrate banking stress in two places: variable cloud and GPU spend (AWS, Google Cloud, Azure bills that spike before revenue) and unusually large raises that need coverage and yield from day one. That favors platforms with high-limit corporate cards and AP automation for the spend side, and strong FDIC sweep coverage plus treasury yield for the raise: Rho offers all four in one platform (savings coverage up to $75 million via a 400+ bank sweep network; treasury up to 4.55% as of 08/02/2026), while Mercury and Brex are also common AI-stack choices. Traditional banks like Chase appear in AI-banking recommendations mostly on relationship strength — compare them on the same fee, coverage, and yield numbers in the table above.